The market for physical gold

In February 1972 the Fed Funds rate was 3.29%, rising eventually to over 19% in January 1981. At the same time gold rose from $46 to a high of $843 at the morning fix on 21 January 1980. Taking gold’s originary interest rate as approximately 2% it required a 17% interest rate penalty to dissuade people from hoarding gold and to hold onto dollars instead.

In 1971, US Government debt stood at 35% of GDP and in 1981 it stood at 31%. The US Government ran a budget surplus over the decade sufficient to absorb the rising interest cost on its T-bill obligations and any new Treasury funding. America enters 2020 with a debt to GDP ratio of over 100%. Higher interest rates are therefore not a policy option and the US Government, and the dollar, are ensnared in a debt trap from which the dollar is unlikely to recover.

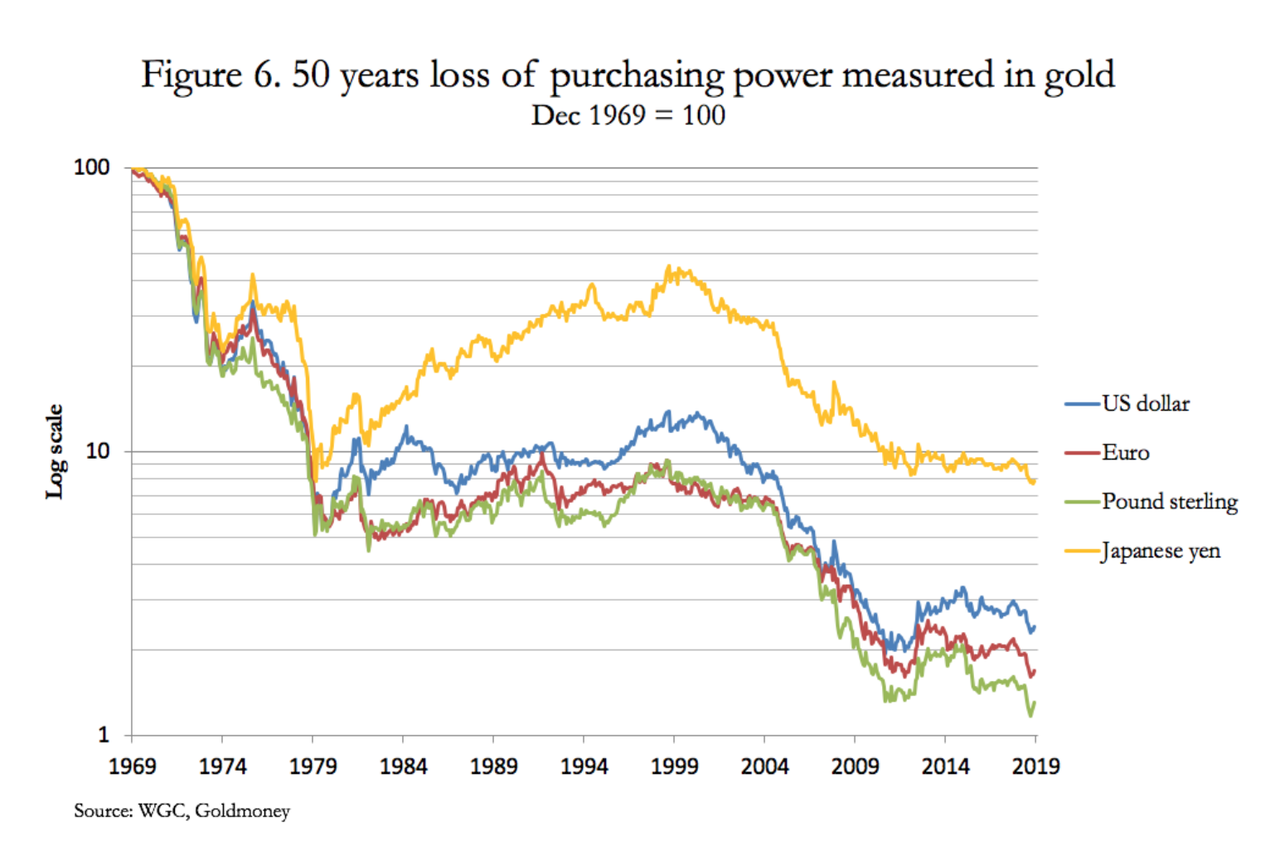

The seeds of the dollar’s destruction were sown over fifty years ago, when the London gold pool was formed, whereby central banks committed to help the US maintain the price at $35, being forced to do so because the US could no longer supress the gold price on its own. And with good reason: Figure 6 shows how the last fifty years have eroded the purchasing power of the four major currencies since the gold pool failed.

Over the last fifty years, the yen has lost over 92%, the dollar 97.6%, the euro (and its earlier components 98.2% and sterling the most at 98.7%. And now we are about to embark on the greatest increase of global monetary inflation ever seen.

The market for physical gold

In recent years, demand for physical gold has been strong. Chinese and Indian private sector buyers have to date respectively accumulated an estimated 17,000 tonnes (based on deliveries from Shanghai Gold Exchange vaults) and about 24,000 tonnes (according to WGC Director Somasundaram PR quoted in India’s Financial Express last May).

It is generally thought that higher prices for gold will deter future demand from these sources, with the vast bulk of it being categorised as simply jewellery. But this is a western view based on a belief in objective values for government currencies and subjective prices for gold. It ignores the fact that for Asians, it is gold that has the objective value. In Asia gold jewellery is acquired as a store of value to avoid the depreciation of government currency, hoarded as a central component of a family’s long-term wealth accumulation.

Therefore, there is no certainty higher prices will compromise Asian demand. Indeed, demand has not been undermined in India with the price rising from R300 to the ounce to over R100,000 today since the London gold pool failed, and that’s despite all the government disincentives and even bans from buying gold.

Additionally, since 2008 central banks have accumulated over 4,400 tonnes to increase their official reserves to 34,500 tonnes. The central banks most active in the gold market are Asian, and increasingly the East and Central Europeans.

There are two threads to this development. First there is a geopolitical element, with Russia replacing reserve dollars for gold, and China having deliberately moved to control global physical delivery markets. And second, there is evidence of concern amongst the Europeans that the dollar’s role as the reserve currency is either being compromised or no longer fit for a changed world. Furthermore, the rising power of Asia’s two hegemons continues to drive over two-thirds of the world’s population away from the dollar towards gold.

The market for physical gold

Reviewed by romania

on

tháng 1 05, 2020

Rating:

Reviewed by romania

on

tháng 1 05, 2020

Rating:

Reviewed by romania

on

tháng 1 05, 2020

Rating:

Không có nhận xét nào