In recent years, the Fed’s attempt to return

In recent years, the Fed’s attempt to return to monetary normality by reducing its balance sheet has failed miserably. After a brief pause, the fiat money quantity has begun to grow at a pace not seen since the immediate aftermath of the Lehman crisis itself and is back in record territory. Figure 1 is updated to 1 November, since when FMQ will have increased even more.

In order to communicate effectively the background for the relationship between gold and fiat currencies in 2020 it is necessary to put the situation as plainly as possible. We enter the new decade with the highest levels of monetary ignorance imaginable. It is a systemic issue of not realising the emperor has no clothes. Consequently, markets have probably become more distorted than we have ever seen in the recorded history of money and credit, as widespread negative interest rates and negative-yielding bonds attest. In our attempt to divine the future, it leaves us with two problems: assessing when the tension between wishful thinking in financial markets and market reality will crash the system, and the degree of chaos that will ensue.

The timing is impossible to predict with certainty because we cannot know the future. But, if the characteristics of past credit cycles are a guide, it will be marked with a financial and systemic crisis in one or more large banks. Liquidity strains suggest that event is close, even within months and possibly weeks. If so, banks will be bailed, of that we can be certain. It will require central banks to create yet more money, additional to that required to finance escalating government budget deficits. Monetary chaos promises to be greater than anything seen heretofore, and it will engulf all western welfare-dependent economies and those that trade with them.

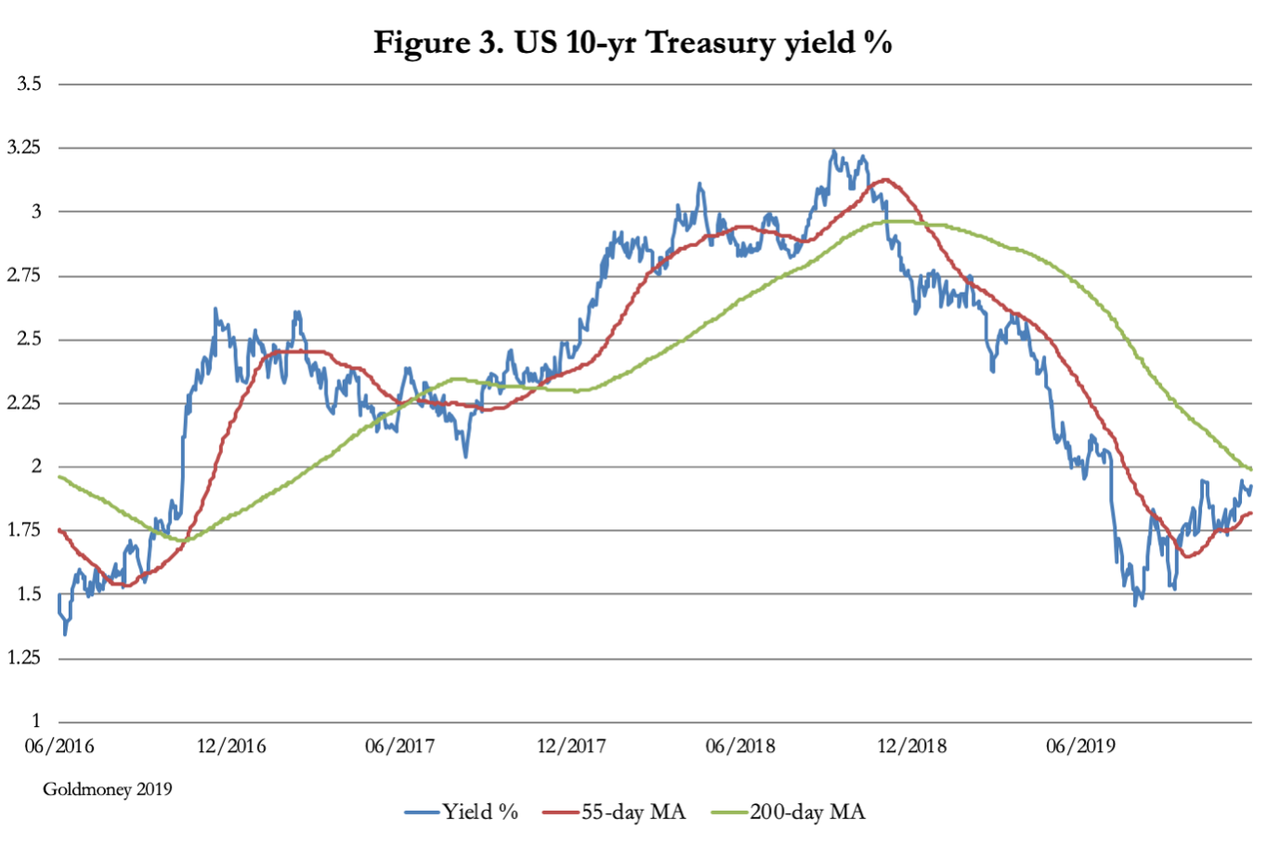

We have established that between keeping governments financed, bailing out banks and perhaps investing in renewable green energy, the issuance of new money in 2020 will in all probability be unprecedented, greater than anything seen so far. It will lead to a feature of the crisis, which may have already started, and that is an increase in borrowing costs forced by markets onto central banks and their governments. The yield on 10-year US Treasuries is already on the rise, as shown in Figure 3.

Assuming no significant increase in the rate of savings and despite all attempts to suppress the evidence, the acceleration in the rate of monetary inflation will eventually lead to runaway increases in the general level of prices measured in dollars. As Milton Friedman put it, inflation [of prices] is always and everywhere a monetary phenomenon.

Through QE, central banks believe they can contain the cost of government funding by setting rates. What they do not seem to realise is that while to a borrower interest is a cost to set against income, to a lender it reflects time-preference, which is the difference between current possession, in this case of cash dollars, and possession at a future date. Unless and until the Fed realises and addresses the time preference problem, the dollar will lose purchasing power. Not only will it be sold in the foreign exchanges, but depositors will move to minimise their balances and creditors their ownership of debt.

In recent years, the Fed’s attempt to return

Reviewed by romania

on

tháng 1 05, 2020

Rating:

Reviewed by romania

on

tháng 1 05, 2020

Rating:

Reviewed by romania

on

tháng 1 05, 2020

Rating:

Không có nhận xét nào