Alasdair Macleod's Gold Outlook For 2020

This article is an overview of the economic conditions that will drive the gold price in 2020 and beyond. The turn of the credit cycle, the effect on government deficits and how they are to be financed are addressed.

In the absence of foreign demand for new US Treasuries and of a rise in the savings rate the US budget deficit can only be financed by monetary inflation. This is bound to lead to higher bond yields as the dollar’s falling purchasing power accelerates due to the sheer quantity of new dollars entering circulation. The relationship between rising bond yields and the gold price is also discussed.

It may turn out that the recent extraordinary events on Comex, with the expansion of open interest failing to suppress the gold price, are an early recognition in some quarters of the US Government’s debt trap.

The strains leading to a crisis for fiat currencies are emerging into plain sight.

Introduction

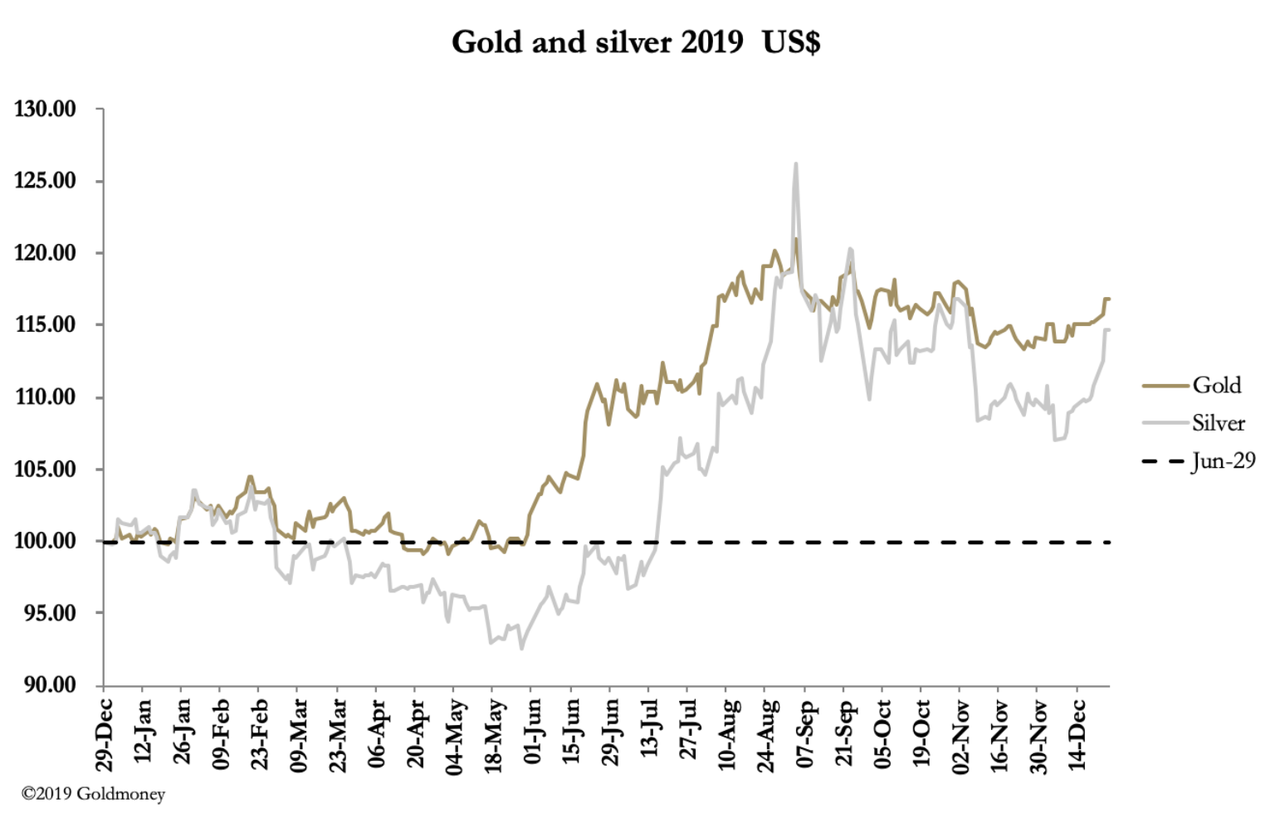

In 2019, priced in dollars gold rose 18.3% and silver by 15.1%. Or rather, and this is the more relevant way of putting it, priced in gold the dollar fell 15.5% and in silver 13%.

This is because the story of 2019, as it will be in 2020, was of the re-emergence of fiat currency debasement. Particularly in the last quarter, the Fed began aggressively injecting new money into a surprisingly illiquid banking system through repurchase agreements, whereby banks’ reserves at the Fed are credited with cash loaned in return for T-bills and coupon-bearing Treasuries as collateral. Furthermore, the ECB restarted quantitative easing in November, and the Bank of Japan stands ready to ease policy further “if the momentum towards its 2% inflation target comes under threat” (Kuroda – 26 December).

The Bank of Japan is still buying bonds, but at a pace which is expected to fall beneath redemptions of its existing holdings. Therefore, we enter 2020 with money supply being expanded by two, possibly all three of the major western central banks. Besides liquidity problems, the central bankers’ nightmare is the threat that the global economy will slide into recession, though no one will confess it openly because it would be an admission of policy failure. And policy makers are also terrified that if bankers get wind of a declining economy, they will withdraw loan facilities from businesses and make things much worse.

Of the latter concern central banks have good cause. A combination of the turn of the credit cycle towards its regular crisis phase and Trump’s tariff war has already hit international trade badly, with exporting economies such as Germany already in recession and important trade indicators, such as the Baltic dry index collapsing. No doubt, President Trump’s most recent announcement that a trade deal with China is ready for signing is driven by an understanding in some quarters of the White House that over trade policy, Trump is turning out to be the turkey who voted for Christmas. But we have heard this story several times before: a forthcoming agreement announced only to be scrapped or suspended at the last moment.

The subject which will begin to dominate monetary policy in 2020 is who will fund escalating government deficits. At the moment it is on few investors’ radar, but it is bound to dawn on markets that a growing budget deficit in America will be financed almost entirely by monetary inflation, a funding policy equally adopted in other jurisdictions. Furthermore, Christine Lagarde, the new ECB president, has stated her desire for the ECB’s quantitative easing to be extended from government financing to financing environmental projects as well.

2020 is shaping up to be the year that all pretence of respect for money’s role as a store of value is abandoned in favour of using it as a means of government funding without raising taxes. 2020 will then be the year when currencies begin to be visibly trashed in the hands of their long-suffering users.

Gold in the context of distorted markets

At the core of current market distortions is a combination of interest rate suppression and banking regulation. It is unnecessary to belabour the point about interest rates, because minimal and even negative rates have demonstrably failed to stimulate anything other than asset prices into bubble territory. But there is a woeful lack of appreciation about the general direction of monetary policy and where it is headed.

Alasdair Macleod's Gold Outlook For 2020

Reviewed by romania

on

tháng 1 05, 2020

Rating:

Reviewed by romania

on

tháng 1 05, 2020

Rating:

Reviewed by romania

on

tháng 1 05, 2020

Rating:

Không có nhận xét nào